Financing Alone: Money Management in College

CW/ Autumn Williams

August 8, 2022

Unless you are a finance student, talking about money isn’t an easy topic. Among talk of a looming recession, rising inflation and high gas prices, starting college and taking finances into your own hands can appear to be a massive burden, especially if most financial talk sounds like a foreign language.

According to a 2019 study by the Financial Industry Regulation Authority, over 50% of American adults are not adequately saving money, and financial literacy rates have dropped to only 34% — with participants only being able to answer four or five financial questions. Along with this, nearly 50% of adults with student loans regret the price of their education. However, the study also concluded that nearly 50% of participants saw that with an increase in financial literacy comes increased savings.

The University of Alabama offers free access to the Higher Education Financial Wellness Alliance’s CashCourse program, which provides courses on budgeting, loans, saving and more, as well as budgeting tools and resources to make your financial journey a little more digestible. They also have tests before and after the lesson in order to gauge progress.

Christopher Whaley, a clinical professor of finance at The University of Alabama, said budgeting isn’t just about saving money; remaining goal-minded is key.

“You need to have a goal in mind when building your budget or an investment strategy: some stated outcome that is specific, measurable and bounded within a period of time. Cliched plans to ‘get rich’ or ‘have more money’ are too broad to effectively manage your finances,” Whaley said. “These could be anything from, ‘pay off my student debt 5 years after graduation’ or ‘buy a house when I am 25’ or ‘a net worth of $1,000,000 by 35,’ something that you have put thought behind and can develop a strategy to achieve.”

While goals make financial successes feel more tangible, starting out can still be a grueling task.

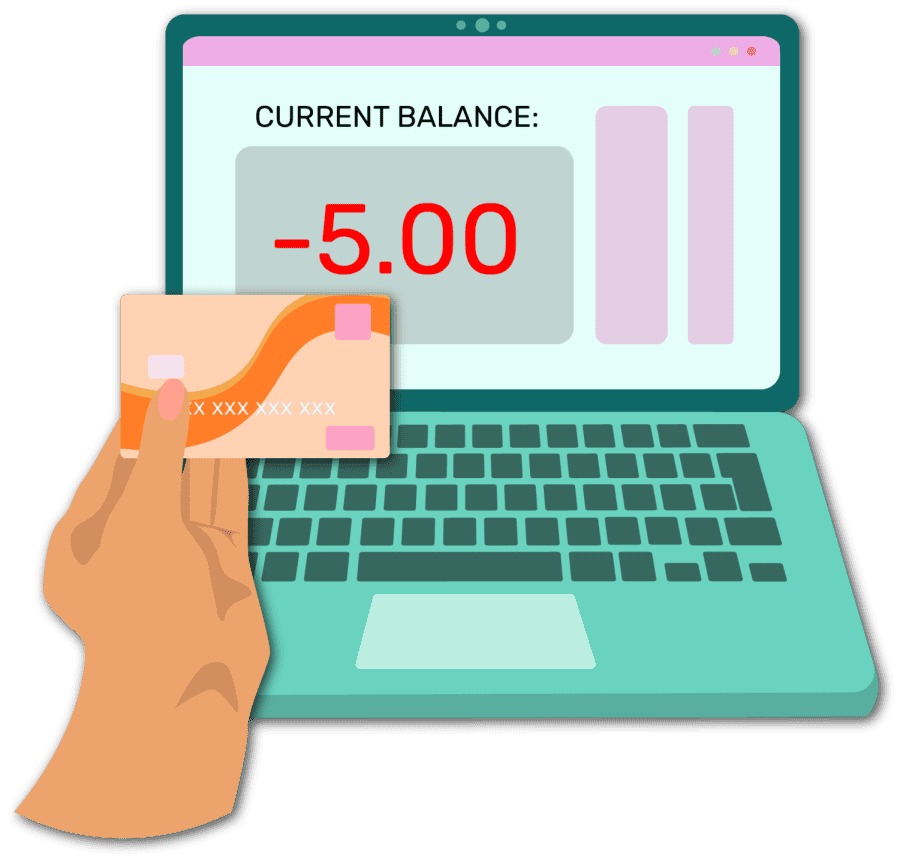

To start budgeting, keep track of a few weeks of spending. It’s important not to overthink it, spend as normal. Instead of sifting through bank statements, plenty of free apps like Mint exist to track these expenses automatically. After adding your bank accounts, credit cards, investments and other assets, Mint shows you graphs of your income and lets you know when spending increases or decreases.

Though mind-numbing to some, it’s important to budget and be aware of your current financial situation. Knowing how much money you have in the bank, investments and income provides a baseline to work off for budgeting. Everyone has different financial situations; some students can act blasé knowing they have a family safety net, but other students may need to pick up numerous jobs in order to pay rent, buy groceries and handle living expenses. Either way, knowing how much can be spent and what expenses must be paid is crucial.

“No matter how good or bad, comfortable or scary it might be, knowing where you are financially and how you are spending your money is a great step,” Whaley said.

It’s not uncommon to be stressed when taking steps to assess your financial situation, as nearly half of the adults surveyed by FINRA reported stress due to simply thinking about their finances. However, it’s necessary in order to secure a comfortable future and retirement.

The 50/30/20 rule can make this easier, as they provide a starting point to saving. With this plan, 50% of income would go towards needs, such as bills, 30% towards wants and the remaining 20% towards savings. When starting off, reaching this balance may be difficult, so don’t be afraid to tweak it towards something that works for you, such as 70/10/20.

While savings may seem boring, as it gains less interest than investing, there is good reason to keep savings.

“Keep a ‘rainy day’ fund of 3-6 months of salary for unexpected events like the loss of a job, a sudden move or other unforeseen circumstances,” Whaley said.

It’s easy to fall into a routine of eating out every night, but even the cheapest fast-food options add up. Although dining hall food isn’t always appetizing, it’s smart to make use of the meal plan you’re required to purchase. However, if dining hall food isn’t cutting it, try planning meals and grocery shopping to cut down on expensive takeout.

Investing may also be foreign, but it doesn’t have to be hard. Find a brokerage that offers commission free trading, which means you don’t have to pay anything whenever you purchase a stock. While day-trading and cryptocurrency have taken the forefront with social media, planning and investing for retirement is recommended by almost everyone. Starting an Individual Retirement Account , coupled with smart investments regularly, can help build towards retirement goals.

Whaley said understanding your investments is non-negotiable.

“Make sure whatever you invest in, be that a savings account, stocks or cryptocurrencies, [that you] know how it works or how it makes money. If you cannot explain it in a simple way, you probably do not understand it and should not be investing in it,” Whaley said. “Our department, our college and our university provide numerous opportunities to expand your financial literacy.”

Now that adulthood has reared its ugly head, the thought may cross your mind to finally get your own credit card. Maybe that CapitalOne envelope arrived at your door, paired with a mockup credit card just asking to have a place in your wallet. Credit is not something you should take lightly, and just because you’re “pre-approved” doesn’t mean you should immediately go online and apply. Many cards like these have exorbitantly high interest rates and hidden fees, meaning you end up paying more than you need.

While credit naysayers warn against their abuse, it can be a powerful tool when used properly. Building a high credit score can grant access to more attractive rates on home and car loans, and access to higher tier credit cards that grant cashback and airline miles, along with other savory benefits.

The most important facet to credit card usage is personal responsibility. Being able to charge to a card with no worry of what is in your bank account is tempting, but it’s important to still only spend what you have available. Think of a credit card no different than a debit card and stay on top of spending. Putting recurring charges like a Netflix subscription on your credit card can help cement your credit worthiness, but only by staying on top of payments.

Financial planning is stressful, so don’t let it eat you alive. Sticking to a budget and cutting excess spending are important to that journey, but it can’t solely dictate your life. While you can’t live without money, you can’t be miserable either, so don’t stop yourself from splurging on a new toy or dinner with friends occasionally.

To quell the fears of finance, Whaley leaves a final, positive point to personal finance.

“When we talk about personal finance, we attend mostly to the finance-side of that topic and put little emphasis on the personal. But that is exactly what it is, personal,” Whaley said. “It is an opportunity for you to show not only your responsibility, but your independence as well.”